- April 4, 2026

- Mark Elwes

How Emergency Loans Work in the UK and What to Know Before Applying?

Table of Contents

Quick financial solutions become essential when unexpected costs strike your budget hard. You could be dealing with motor repairs, damaged house fittings or health expenses. Emergency loans offer instant cash to deal with these emergencies.

Many lenders now offer emergency loans in the UK for bad credit.This is more about your present capability to pay back than previous monetary errors. These loans assist in situations where mainstream banks have said NO, and the application is simplified to enable quick decisions in times of stress.

How to Choose the Right Emergency Loan?

This takes a little comparison to find the best alternative. You will find that even with tight time constraints, a few minutes of shopping around will help.

Step 1: Don’t just look at the rates you see on the headline, but the real repayment figure. The lowest APR is not necessarily the cheapest one since there are different types of loans. You can add all the repayments and fees together and determine the amount you will actually repay.

Step 2: Ensure any lender is well-regulated and licensed by the FCA (Financial Conduct Authority). This will save you from a scam and unfair treatment. The FCA register allows you to verify this in a fast and online version before you provide any personal information.

Many borrowers with troubled credit histories can apply for very bad credit loans with no guarantor from a direct lender. These offer accessible options in times of need. The direct lenders tend to be far more liberal with their loan criteria. You can give you access to funds when you need them most.

Step 3: Many individuals post their reviews on review sites such as Trustpilot. You can look for patterns in the feedback rather than just isolated complaints or praise.

Step 4: Figure out whether you can pay when you have surplus cash. There are lenders that collect fees on early repayment, and some lenders are okay with it.

Step 5: Select a payment plan that best meets your funds available at the end of the month. You should be honest with yourself about what you can afford each month without creating new financial problems.

Types of Emergency Loans Available in the UK

There are several possibilities when you require the cash quickly, based on the case at hand.

Payday Loans

These offer short-term fixes, where you can usually borrow up to £1,000. You will pay it back with interest, the next time you earn a wage. You can do the application within minutes, and the cash can be in your account several hours later.

Guarantor Loans

The guarantor loans require someone to back your application for larger amounts up to £15,000. This individual (a member of your family or a friend) often agrees to pay your debt in case you are unable to do so. The payment terms range between one and five years.

Doorstep Loans

These also go by the name of home collection loans, and the money is actually taken to your door. The agent goes out to make cash payments and comes back weekly to collect repayments. This is useful when you want to chat, rather than fill out the forms, online.

Bank Overdrafts

Your current bank can possibly permit you to spend beyond the money you have in your account. This generates an overdraft, which is used as a loan in itself. The arranged overdrafts have agreed limits and fees.

Credit Card Cash Advances

You can take actual cash out of ATMs with a credit card already in possession. The interest starts immediately with no interest period, as opposed to regular card purchases. There are usually other handling charges.

| Red Flags vs Legitimate Lenders | |

| Warning Signs | Legitimate Lenders |

| Not on FCA register | FCA authorised number displayed |

| Upfront fees required | No fees until loan approved |

| Guaranteed approval claims | Proper affordability checks |

| No credit checks mentioned | Appropriate credit assessment |

| Contact via social media only | Professional website and phone |

| Pressure to borrow maximum | Encourage responsible borrowing |

| No cooling-off period | 14-day withdrawal rights |

| Unlicensed debt collection | Follow FCA collection guidelines |

What to Know Before Applying for Emergency Loans?

Simple borrowing begins with you knowing what you are getting into.

Eligibility Requirements

Before giving you funds, lenders must verify that you satisfy the following basic requirements:

- You should have been a resident of the UK for three months or more.

- Age requirements are important, as you must be 18 and above.

- Regular income proves you can repay, whether from a job or benefits.

- Transactions are conducted by an active UK bank account containing a direct debit facility.

- The affordability checks apply to your income and expenses.

- The documents, such as recent payslips or bank statements, confirm this case.

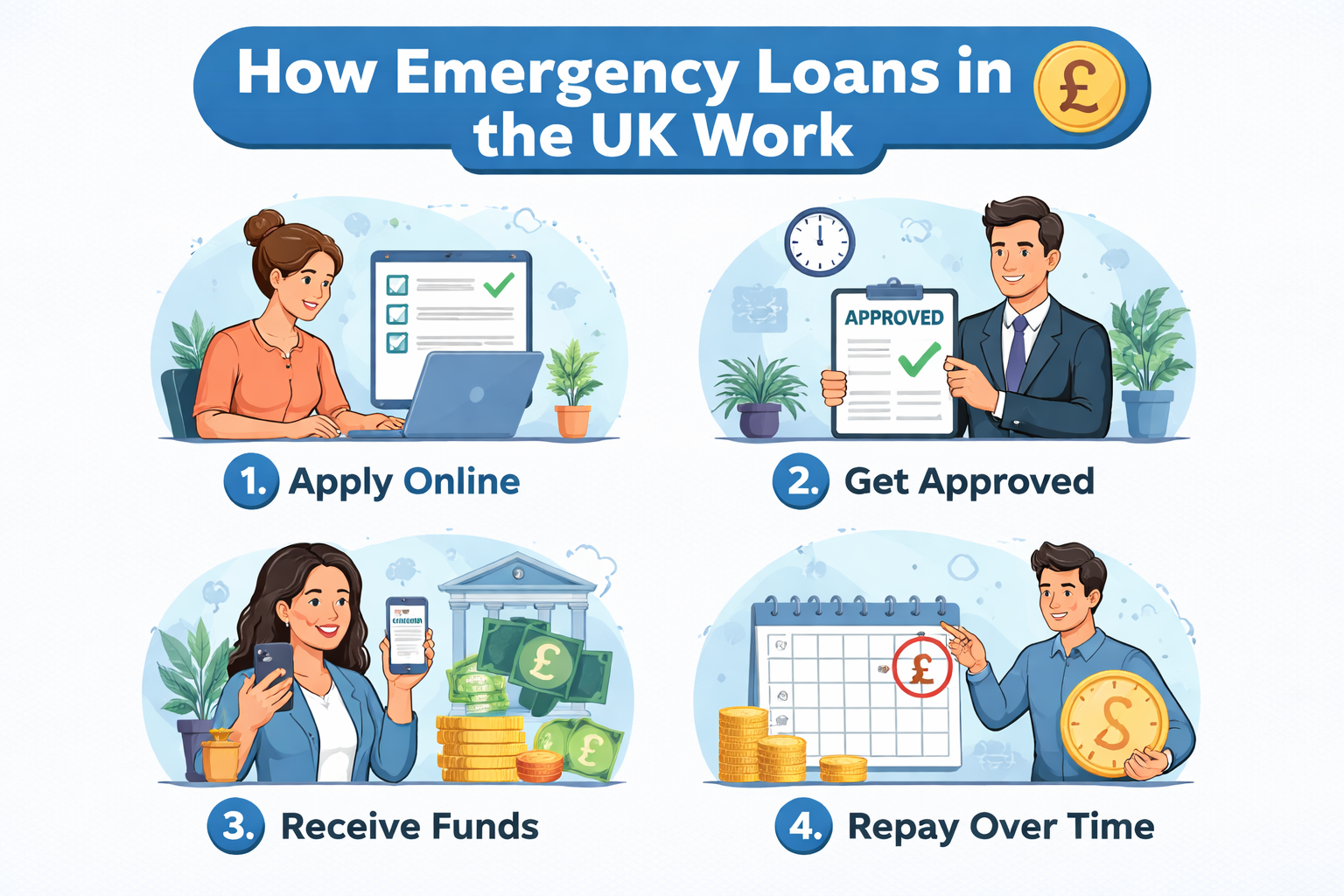

Application Process and Speed

Application-to-cash is a time-tested process:

- Online forms require 5-15 minutes to fill out.

- Many lenders provide instant decisions through automated systems.

- Mostly, money appears in your account the same day or within a day.

- Bank transfers are quicker than ancient cheques.

- Weekend applications could be left till Monday.

- Phone calls often verify your identity before final approval.

Costs and Interest Breakdown

It is most important to know the price tag:

- There is a wide range of APR figures, with some lenders offering more than 1500% with others offer less.

- Payday loan interest cannot exceed 0.8% per day as required by the FCA.

- Consumer protection total costs are limited to 100 per cent of the amount borrowed.

- There is a limit of up to £15 on late payment fees should you miss a payment date.

- You could save by paying early and saving on upfront interest.

Building an Emergency Fund After Repayment

The easiest solution to the problems of the future is to prevent lending. After debts are paid, it is time to create your safety net. You can start by saving between £10-50 each month once you have paid off your loan.

The target should be £500-£1000 as your starting emergency cushion. This includes lots of unforeseen common costs without any borrowing.

Find savings accounts that have reasonable interest rates for your emergency money. Some accounts have a high rate as long as you avoid taking off.

You can install automatic transfers to save the money immediately after payment. The ” pay yourself first rule makes sure that you save and then you spend. You will soon become accustomed to living on what has been moved over to your savings.

Conclusion

Emergency loans should be used wisely and temporarily. They provide the necessary funding, but the funds need to be well organised to be repaid. Only take what you need, you know about every cost, and you scrutinise before you sign.

You could consider saving an emergency fund after you have paid off your loan to carry on with borrowing in the future. Keep in mind that every successful repayment gets you a better credit profile. This paves the way to improved financial prospects in the future.

Mark Elwes is the Editor-in-Chief at Extramilefinance. He is a notable member of the content strategy team since his joining in 2017. Driven by his fondness for the finance industry, he has spent years gathering as much knowledge as possible about various financial products that include loans also. Previously, Mark worked as a senior journalist writer with experience in writing blogs and articles.