- June 29, 2026

- Mark Elwes

How to Apply for a £1,000 Bad Credit Loan in the UK?

Table of Contents

A poor credit score has a way of making everything feel locked. The car fails its MOT, or the boiler quits on the coldest week of the year, and suddenly you need £1,000 sooner rather than later. And the thought that arrives first usually isn’t about the repair. It’s this nagging one: will anyone actually lend to me?

So here’s what’s worth knowing. A weak score doesn’t close every door, not by a long way. Loads of UK lenders look well beyond the number on your file, and £1,000 happens to be one of the easier amounts to get a yes on when your history’s a bit patchy.

What follows is how it works in practice, plus the small print that’s genuinely worth your attention before you commit to anything.

What a £1,000 Bad Credit Loan Actually Is?

Think of it as a personal loan made for people whose record has a few knocks. A missed payment or two. Maybe a default from years ago that still lingers. Or sometimes there’s barely any history at all, just a thin file because borrowing was never really your thing.

And a £1,000 bad credit loan in the UK is a useful number to land on. Low enough that lenders don’t see much risk in it, yet enough to cover most of life’s nasty surprises.

Some things you’ll spot across most of these loans:

- A repayment window that runs anywhere from 3 to 36 months

- No security needed in most cases, so the house and car aren’t on the table

- Fixed payments month to month, so you always know what’s leaving your account

- An APR that sits higher than mainstream rates, which is the lender’s pricing for the extra risk

While you’re comparing, the words to anchor on are affordable bad credit loans. Repayments that actually fit your budget. Not the biggest number a lender’s willing to wave at you.

Can You Genuinely Get Approved With Bad Credit?

Short answer? Yes. And it’s far from rare.

Specialist lenders in this corner of the market don’t just pull your score and wave you off. They want context: your income, your monthly outgoings, and whether the repayments stack up once everything else is accounted for.

None of that guarantees a yes, mind you. But these are the things that tilt it your way. A steady income you can prove. A UK bank account and an address history that doesn’t jump around. Being straight about your circumstances helps too, because inflating what you earn nearly always comes back to bite you. And asking for a figure that matches your actual income, rather than the one you wish you had.

It really does come down to affordability more than anything. Most lenders would much rather hand over £1,000 you’ll repay comfortably than £1,000 that quietly drags you under.

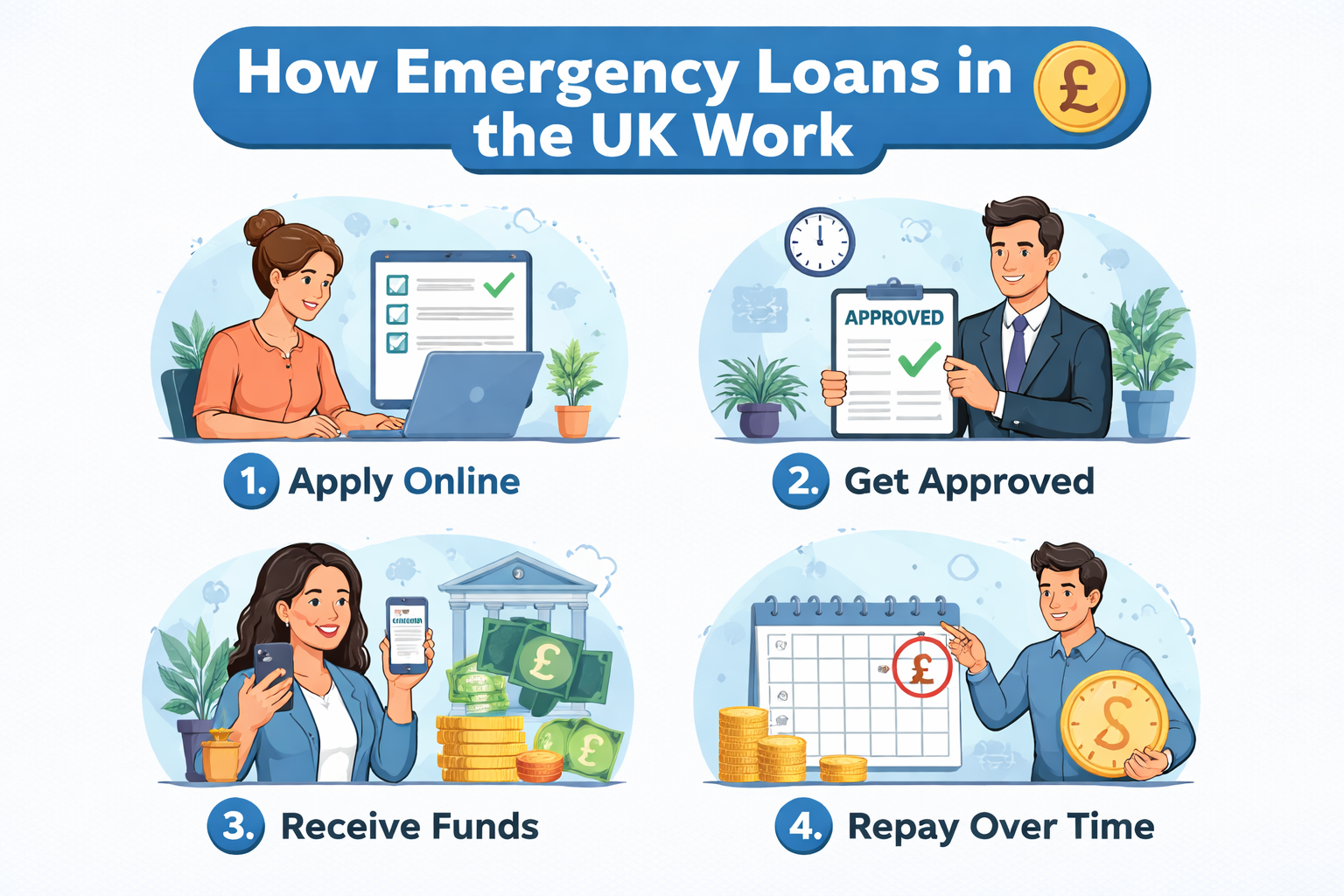

How to Apply: Step by Step!

It’s a fairly quick process, mostly done online, and you’ll often have an answer in minutes.

Step 1 — Pull your credit report. Experian, Equifax and TransUnion all do a free copy. Have a proper look while you’re in there, because the odd error creeps in, and one wrongly logged default can be dragging your score down for no reason.

Step 2 — Be honest about the affordability. Painfully honest, ideally. Income at the top, essential bills underneath, and whatever’s left is your absolute ceiling for repayments. Stay well below it.

Step 3 — Shop around. Compare the representative APR, what you’ll repay in total, and any fees lurking in the details. A low headline rate can still work out dearer overall once it’s all added up.

Step 4 — Run an eligibility check. Most decent lenders have a soft-search tool. It gives you a read on your chances without marking your file, so there’s no harm in using them freely.

Step 5 — Apply. You’ll usually be asked for:

- ID, such as a passport or driving licence

- Proof of where you live, like a utility bill or bank statement

- Something showing income, typically payslips or statements

- Your bank details for the payout

Step 6 — See what they say. A lot of lenders come back instantly or the same day. Get a yes, and the money can be sitting in your account within 24 hours. Sometimes sooner.

What Lenders Usually Expect?

It varies, but as a baseline, most want you to:

- Be 18 or over

- Live in the UK

- Have a regular income coming in

- Hold a UK bank account with a debit card

A handful won’t lend at all if you’ve got an active debt relief order or you’re an undischarged bankrupt. Better to know that going in than to find out at the rejection stage.

Before You Sign: The Bits That Protect You!

A little caution here saves a world of regret later.

First thing: confirm the lender’s authorised. Their register’s online, it takes under a minute, and frankly, it’s the most valuable check on this whole list.

Read the representative APR properly while you’re at it. That advertised rate only has to reach 51% of approved borrowers, so yours might not match it. The personalised quote is the one that counts, not the figure in the window.

A few things should make you stop:

- Being asked for a fee upfront, before the loan’s even granted. Classic scam, that one.

- Any “you need to decide now” pressure

- A lender who seems oddly uninterested in whether you can repay

- No proper address, phone number, or registration anywhere to be seen

The lenders worth dealing with want you to repay without trouble. That’s the whole point of the arrangement, really.

Small Moves That Improve Your Chances!

None of these is dramatic, but together they nudge the odds:

- Register on the electoral roll. Quick to do, and it helps verify who you are.

- Chip away at existing debts where you can; even a little goes a long way

- Don’t scatter applications around all at once. A burst of hard searches close together tends to make lenders nervous.

- Ask for what you need and no more, since over-borrowing reads as less responsible

- Keep your details matching across every form and document

The Honest Truth About Costs!

Higher interest comes with the territory on bad-credit loans. Search for affordable bad credit loans in the UK and maintain your financial goals. That’s just how higher-risk lending works, and no amount of clever shopping makes it disappear entirely.

On £1,000, the total you hand back will almost certainly top what you borrowed once interest is in the mix. So always check that total repayable figure before signing, because it shows you the real cost in actual pounds rather than a percentage that’s easy to gloss over.

And if the numbers feel tight even on paper? That’s your signal to stop and rethink. A loan’s meant to fix a problem, not become one.

Frequently Asked Questions!

- Can I get a £1,000 loan with no credit check? I’d be cautious with anyone promising that. A responsible lender always checks something, even if it’s just a soft search. “No checks at all” isn’t a perk; it’s a warning.

- How fast will the money come through? Usually, within a day of approval. Same day, occasionally, depending on the lender and how quick your bank is.

- Does applying damage my credit score?

A soft check, no. A full application does leave a hard mark, so it’s worth being reasonably sure before you go ahead. - And if I get turned down?

Don’t rush straight into another application. Find out the reason, sort what you can, then give it a bit of breathing room before trying somewhere else.

Final Thoughts

When money’s tight and time’s against you, a £1,000 bad credit loan can genuinely take the pressure off, as long as you walk in clear-eyed about it.

Keep to authorised lenders. Only borrow what you know you can repay. And read every number before you put your name to anything. Get those right, and what felt like a crisis turns back into something you can handle.

Mark Elwes is the Editor-in-Chief at Extramilefinance. He is a notable member of the content strategy team since his joining in 2017. Driven by his fondness for the finance industry, he has spent years gathering as much knowledge as possible about various financial products that include loans also. Previously, Mark worked as a senior journalist writer with experience in writing blogs and articles.