- April 2, 2025

- Mark Elwes

What Is a Long-Term Loan and How Do Long-Term Loans Work?

Table of Contents

A loan is generally called a long-term loan when payments are spread over a period of more than five years. Instalment loans with at least a five-year repayment period are secured, meaning you will lose the collateral in case you fail to discharge the debt.

Long-term loans enable you to borrow a large amount of money that you repay in fixed monthly instalments. However, mortgages offer slightly different repayment plans. The fixed interest rate deal lasts until two, three, or five years, after which you are put on a standard variable interest rate. The size of monthly instalments will change as the base rate fluctuates.

Long-term loans are usually employed to make large purchases such as a house, car, bigger renovation project, and destination wedding. To qualify for these loans, you must have a decent credit report and strong repaying capacity. The approval criteria for long-term loans are not the same as for small long-term loans. While it is vital to assess your current financial situation, lenders will estimate your financial condition in the future, too.

How do long-term loans work?

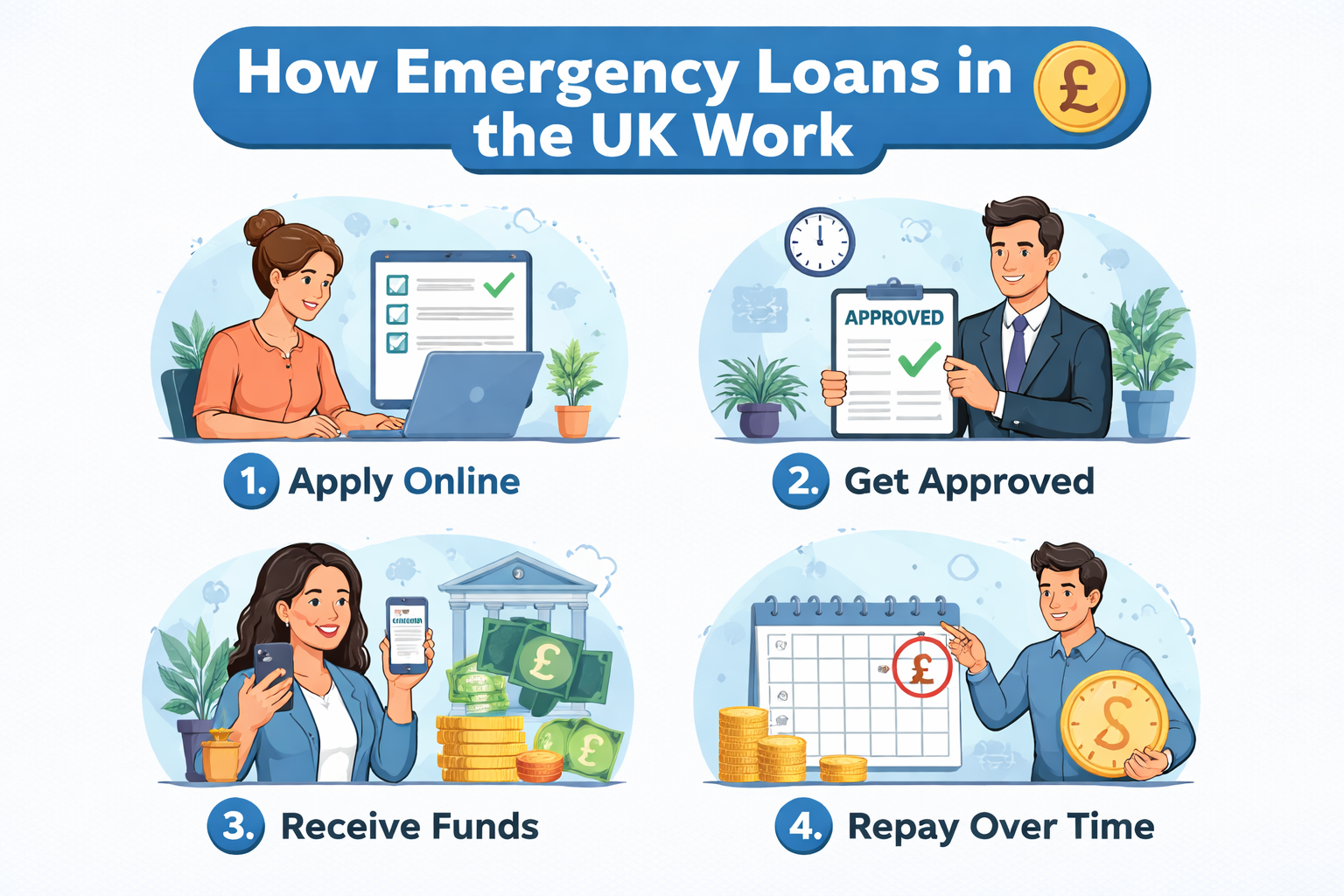

Long-term loans could be applied for from banks and direct lenders. The approval depends on your repaying capacity. Borrowing money from online lenders is hassle-free because you do not have to apply for the loan in person. There are various direct lenders on the market providing these loans. To apply for long-term loans, you need to submit an application online.

The application form varies by lender. Some provide you with an extensive application form that includes particulars about your income, the number of dependents and other details that could influence the decision of a lender. However, some lenders only ask you to fill in your contact details so they can reach you later and discuss what things they need to approbate your application.

A lender would require you to submit a bank statement for the previous six months. In addition, they would want to know the purpose of borrowing money and a pay slip. If you are an entrepreneur, you would need to submit a profit and loss statement. Lenders peruse your income sources to check whether your budget has wiggle room to meet an additional obligation.

Apart from this, they also peruse your credit file. Your credit score should be excellent to increase your chances of being approbated. However, it does not mean that your poor credit score precludes you from submitting your application. There are some lenders who provide long-term loans for bad credit with no guarantor, but they charge higher interest rates. Because bad credit increases the default risk, the loan amount will also be restricted.

Once you receive approval for your application, you will obtain funds directly in your bank account. The loan becomes due as soon as you receive it. This means you will be obligated to pay down the first instalment when it is due.

Make sure you do not miss any payment because late payments will result in late payment fees, mushrooming the cost of the debt. Any default will send your account to the collection agencies, and if you still refuse to discharge your outstanding debt, you will end up with a lawsuit.

Late payments and defaults have far-reaching adverse consequences. Not only will you suffer financially, but you will also lose your credit points. It will make it even more difficult for you to borrow money at lower interest rates down the line.

What benefits do long-term loans offer?

Long-term loans are more manageable than small emergency loans and personal loans. as the whole debt is spread over a number of years, you can easily plan your budget around payments. They also have the ability to borrow a larger sum of money. It will not ruin your budget because payments are spread over a number of years.

Another benefit is that they come with lower interest rates. Small online instalment loans carry high interest rates as they do not last more than six months. If you apply for an emergency loan, you are required to pay it off in fell one swoop. They are even more expensive. If you are applying for these loans with an abysmal credit report, interest rates will likely be extortionate.

Fortunately, this is not the problem with long-term loans. They are much more affordable than small loans. One of the reasons for this is that they are subject to collateral. Usually, your loan will be secured against your house. It reduces the risk of a lender. Interest rates are typically charged high when there is a high risk of default. Despite a poor credit rating, you might qualify for lower interest rates because of collateral. It offsets the impact of your poor credit rating.

What are the drawbacks of long-term loans?

One of the drawbacks of long-term loans is that they are expensive. Though they carry lower interest rates, you will end up paying more interest in total. This is because of an extended repayment period. The longer the repayment term, the smaller the monthly instalment will be. As a result, interest keeps accruing on the unpaid balance. You should always try to ensure that you do not choose an overly extended repayment period.

You cannot be so certain about your finances in years to come. If your income goes up, you would feel inclined to discharge the debt sooner. Doing so will never work in your favour because you will have to pay early repayment charges. If your income goes down, you will face difficulty in the settlement of your debt. Any missed payment or default might result in losing your property. Apart from that, you will lose your credit points.

The final word

Long-term loans are more manageable than small personal loans. As they are subject to collateral, you can avail yourself of lower interest rates. The collateral mitigates the impact of default, and therefore, your chances of qualifying for lower interest rates are high despite a poor credit score. Though these loans are affordable, caution is enjoined while applying for them.

Mark Elwes is the Editor-in-Chief at Extramilefinance. He is a notable member of the content strategy team since his joining in 2017. Driven by his fondness for the finance industry, he has spent years gathering as much knowledge as possible about various financial products that include loans also. Previously, Mark worked as a senior journalist writer with experience in writing blogs and articles.